Most doctors don’t remember choosing their insurance cover.

They remember being told it was standard.

They remember the premium.

They remember signing.

What they rarely remember is the decision hidden inside it.

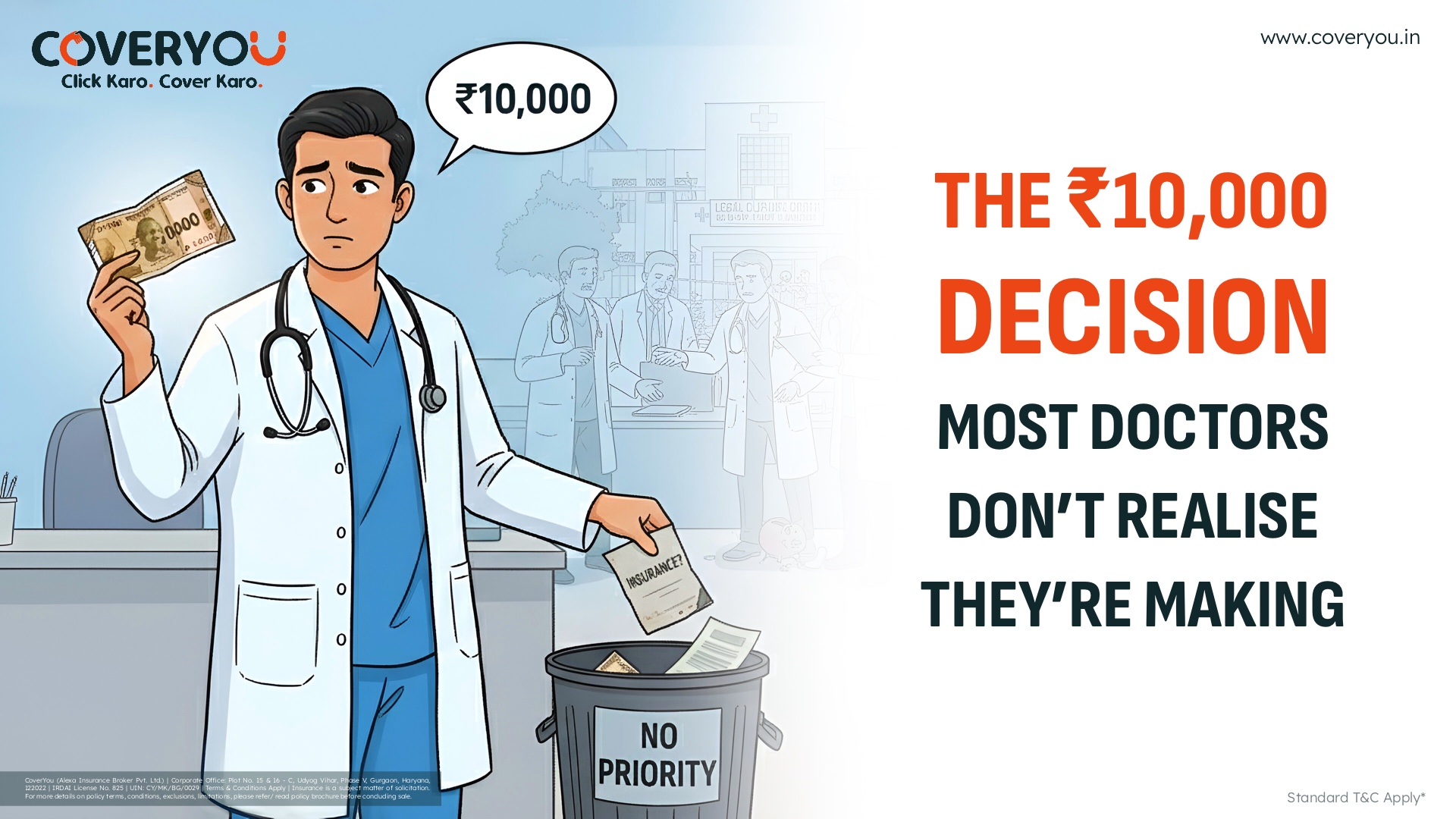

Somewhere in the policy – often unnoticed – sits a number that quietly shapes outcomes: a sub-limit, deductible, or condition that caps responsibility in specific situations.

On paper, it might look minor.

₹10,000. ₹25,000. A percentage. A clause that feels procedural.

In practice, it’s a decision about how much uncertainty a doctor is willing to absorb personally.

This number doesn’t matter when nothing goes wrong. It doesn’t appear in conversations. It doesn’t affect daily practice.

It only becomes visible when a claim is assessed – not rejected, but reduced.

At that point, doctors often feel blindsided.

The policy existed.

The coverage was active.

And yet, part of the responsibility quietly shifted back to them.

This isn’t deception. It’s structure.

Insurance doesn’t ask doctors whether they understood a sub-limit. It assumes acceptance once the policy is issued. The system treats silence as agreement.

Most doctors don’t intentionally choose these limits. They inherit them – through defaults, renewals, or assumptions that last year’s policy is still adequate.

That’s where the real decision happens.

Not at the time of crisis.

At the time of indifference.

₹10,000 doesn’t feel consequential when things are stable. But during a claim, it becomes symbolic – the moment doctors realise that coverage is not binary.

It exists on a spectrum.

Understanding insurance isn’t about knowing every clause. It’s about recognising which small numbers carry disproportionate weight.

Because insurance outcomes are rarely decided by large declarations.

They are decided by small decisions that didn’t feel like decisions at the time.

End.